Which of the Following Is True Concerning Purely Competitive Industries

Other firms will enter this industry. There will be economic losses in the long run because of.

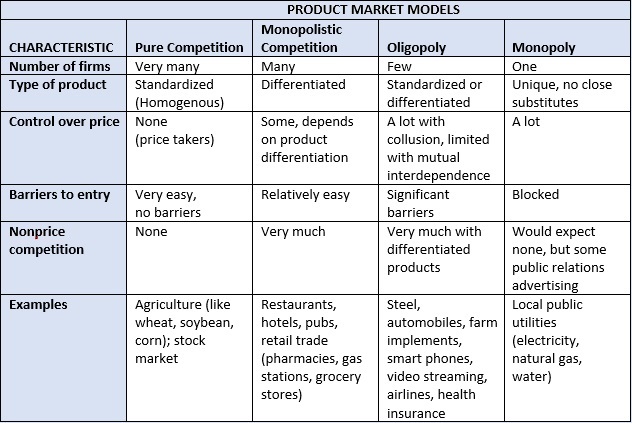

Pure Competition

Answers 1 A is the correct answer.

. B marginal revenue equals marginal cost. In the modern economy there are different industries and for economic analysis the industries are divided into four models based on the amount of competition in the markets the four types are Pure competition oligopoly monopolistic competition and pure monopoly. In the short run firms may incur economic losses or.

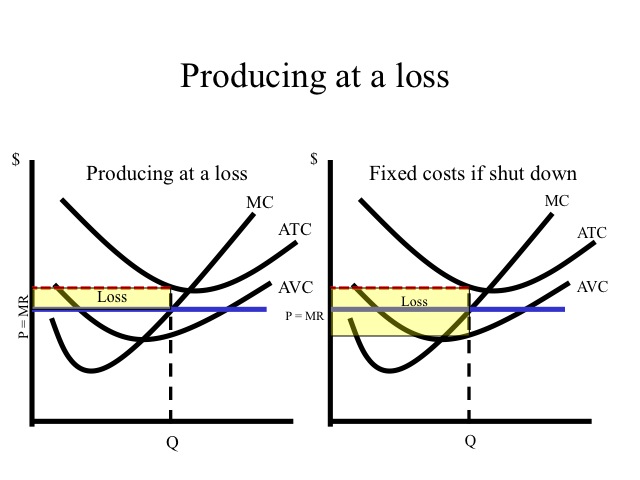

There will be economic losses in the long run because of cut-throat competition. B No Firm has an incentive either to enter or exit the industry. In the short run firms may incur economic losses or.

Open which of the following is true concerning purely competitive industries There will always be economic losses in the long run because. Economic profits earned by firms already in the industry. There will be economic losses in the long run because of cut-throat competition.

C The price of the product is such that the quantity supplied by the industry is equal to the quantity demanded by Consumers. The primary force encouraging the entry of new firms into a purely competitive industry is. Government subsidies for start-up firms.

Economic profits will persist in the long run if consumer demand. There will be economic losses in the long run because of cut-throat competition. Which of the following is true concerning purely competitive industries.

Some existing firms in this market will leave. D all of these are true. Which of the following is true in the long run concerning purely competitive industries.

Which of the following is true concerning purely competitive industries. For unlimited access to Homework Help a Homework subscription is required. 13 When a perfectly competitive firm is in long - run equilibrium.

New firms will enter this market. A long run Competitive equilibrium of a perfectly competitive industry occurs when. Demand is strong and stable.

Increase output to increase price to decrease and profits to decrease. Which of the following is true concerning purely competitive industries. Tutorial 00571255 Puchased By.

Firms can earn economic profits in the long run if the long-run supply curve is upward sloping. There is no tendency for the firms industry to expand or contract D. 500 400.

Economic profits will persist in the long run if consumer. The selling price for this firm is above the market equilibrium price. 14 A perfectly competitive firm industry.

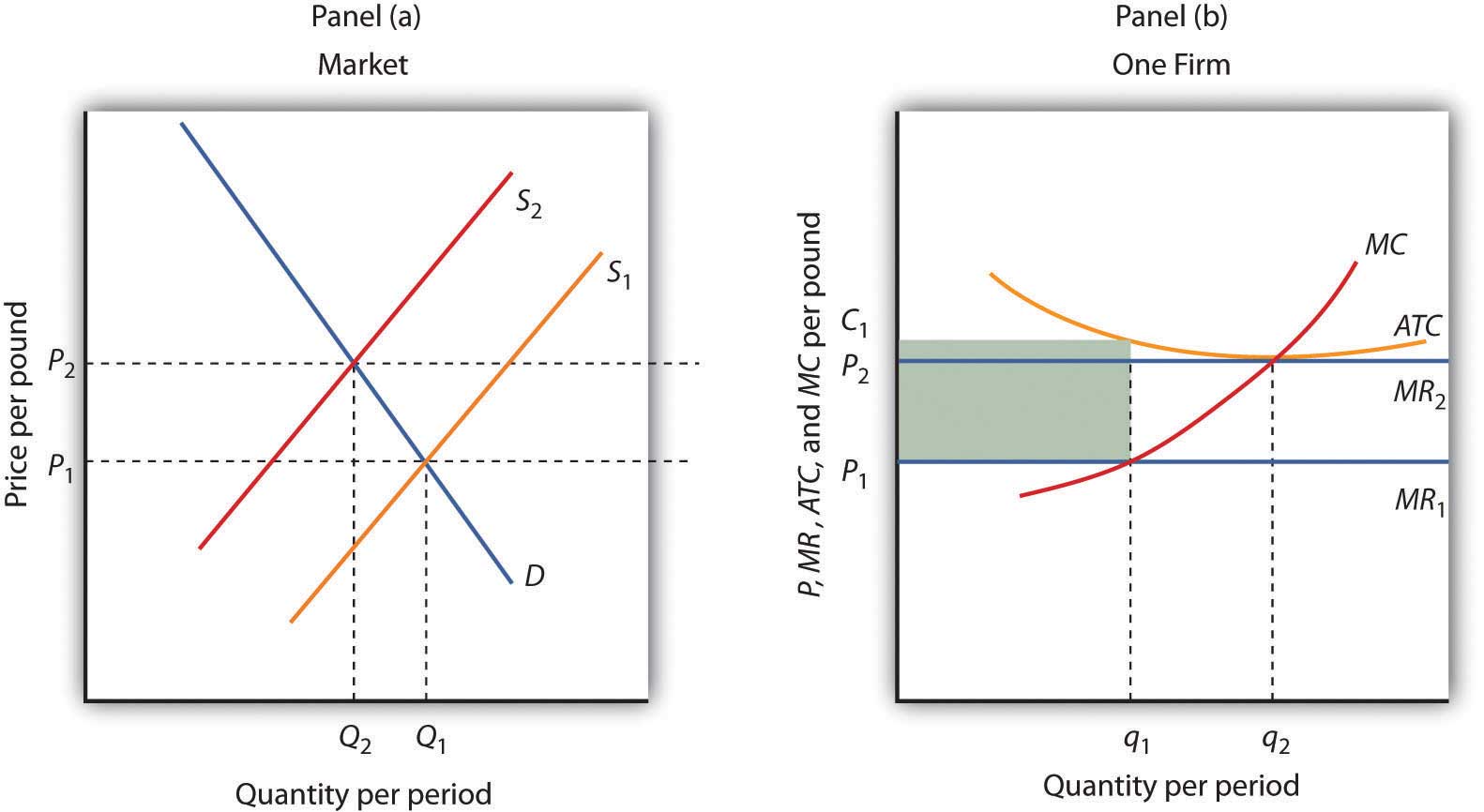

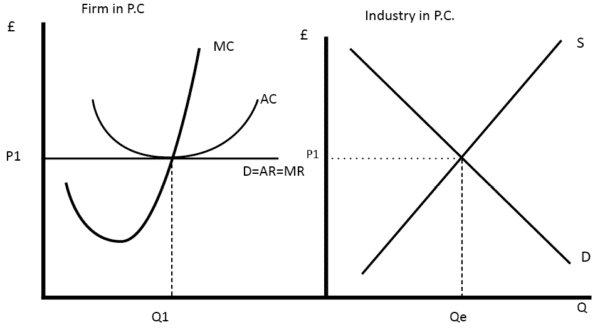

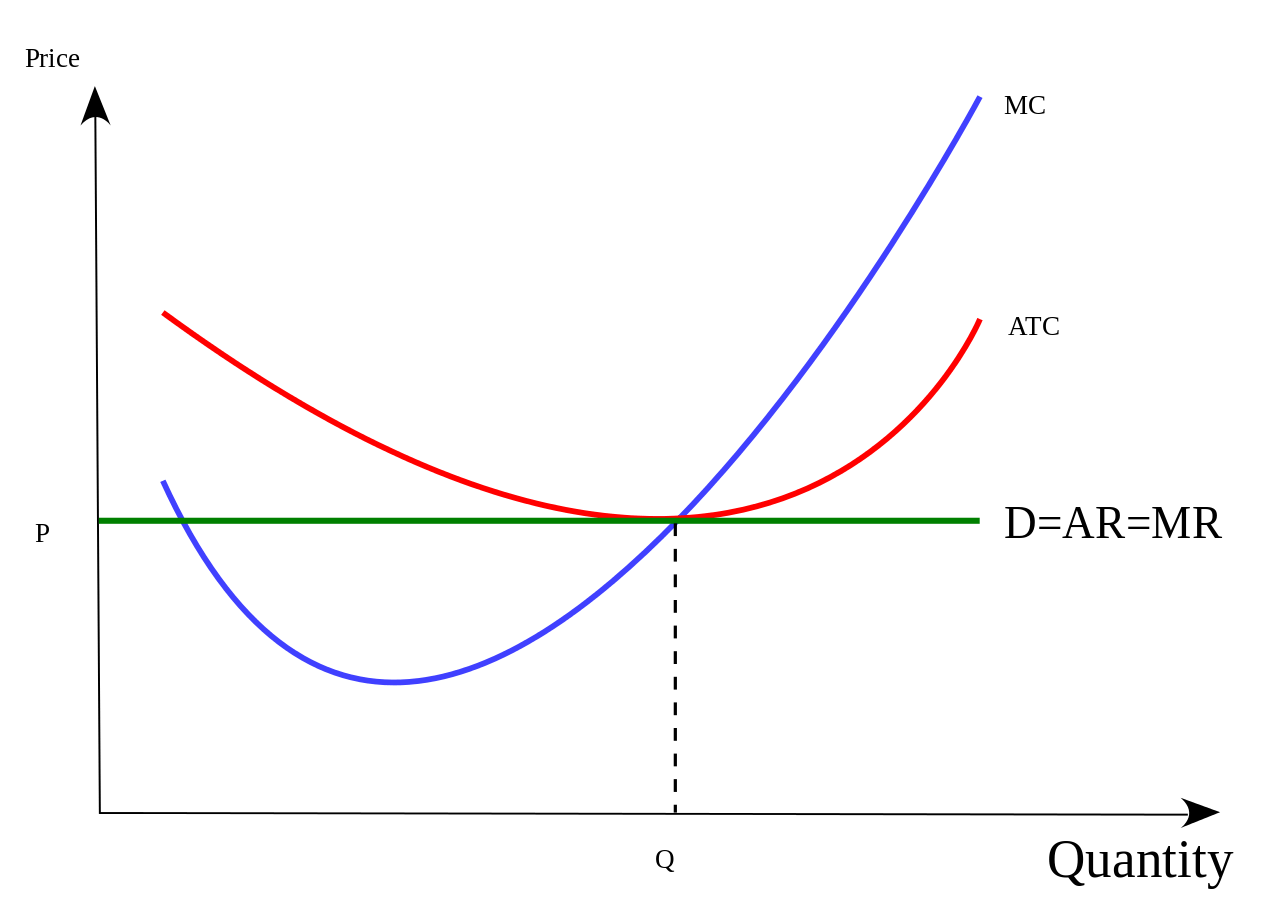

As they all state true and essential characteristics that are necessary to make an industry perfectly competitive. Free entry and free exit into the market require that firms earn zero economic profit in the long run even though they may be able to earn economic profits in the short run. Because for purely competitive firms marginal revenue price maximum revenue is also earned when the marginal cost of producing the last unit equals the market price.

A All Firms in the industry are in equilibrium. BA perfectly competitive industry. If a purely competitive firm is producing at the MR MC output level and earning an economic profit then.

Option ABD are incorrect. Allocative but not productive efficiency is being achieved C. Pure price competition within some industry means that there must be a no product differentiation b free entry and exit from the industry c zero economic profit in the short run d a great deal.

C minimum average total cost equals price. This makes sense since if the marginal cost was greater than the price. Which of the following is true concerning purely competitive industries.

In an economy where firms in most industries are purely competitive firms individual firms in each industry would produce _____ products and have a _____ share of industry output. AA perfectly competitive industry produces more output and charges the same price as a single-price monopoly. Up to 256 cash back In a competitive market with identical firms a.

ECO 2301 - In a purely competitive market which of the following. In the short run firms may incur economic losses or earn economic profits but in the long run they earn normal profits. Only in the pure competition market the competition is very.

Asked Aug 6 2018 in Economics by skiatomic08. Economic profits will persist in the long run if consumer demand is strong and stable. Input prices fall or technology improves as the industry expands.

Economic profits will persist in the long run if consumer demand is strong. The firm is earning an economic profit B. Which of the following is true concerning purely competitive industries.

A price equals marginal cost. A decreasing-cost industry is one in which. Normal profits earned by firms already in the industry.

Get 1 free homework help answer. Already have an account. Assume a purely competitive firm is maximizing profit at some output at which long-run average total cost is at a minimum.

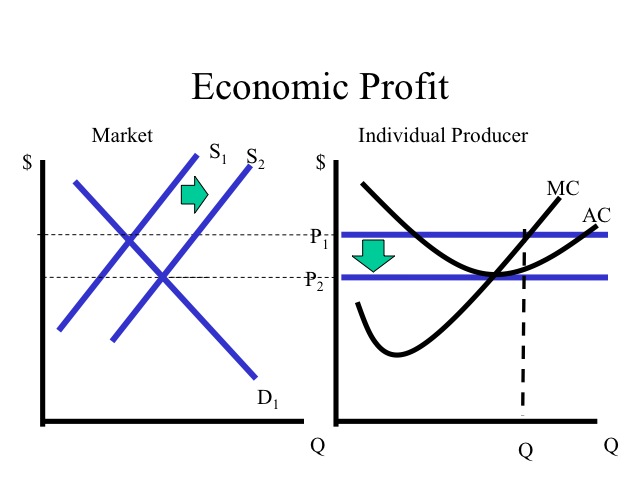

If a purely competitive constant-cost industry is realizing economic profits we can expect industry supply to. Up to 256 cash back Which of the following is not a characteristic of pure competition. Earn economic profits but in the long run they earn normal.

Which of the following is true concerning purely competitive industries.

Pure Competition

Econ 150 Microeconomics

Pure Competition

Market Models Pure Competition Monopolistic Competition Oligopoly And Pure Monopoly

Market Models Pure Competition Monopolistic Competition Oligopoly And Pure Monopoly

Pure Competition

Long Run Economic Profit For Perfectly Competitive Firms Video Khan Academy

Perfect Competition In The Long Run

Pure Competition

Pure Competition

Introduction To Perfect Competition Video Khan Academy

Pure Competition

Perfect Competition Economics Help

Econ 150 Microeconomics

Perfect Competition Definition 5 Characteristics 3 Examples Boycewire

Econ 150 Microeconomics

Pure Competition

Pure Competition

Pure Competition

Comments

Post a Comment